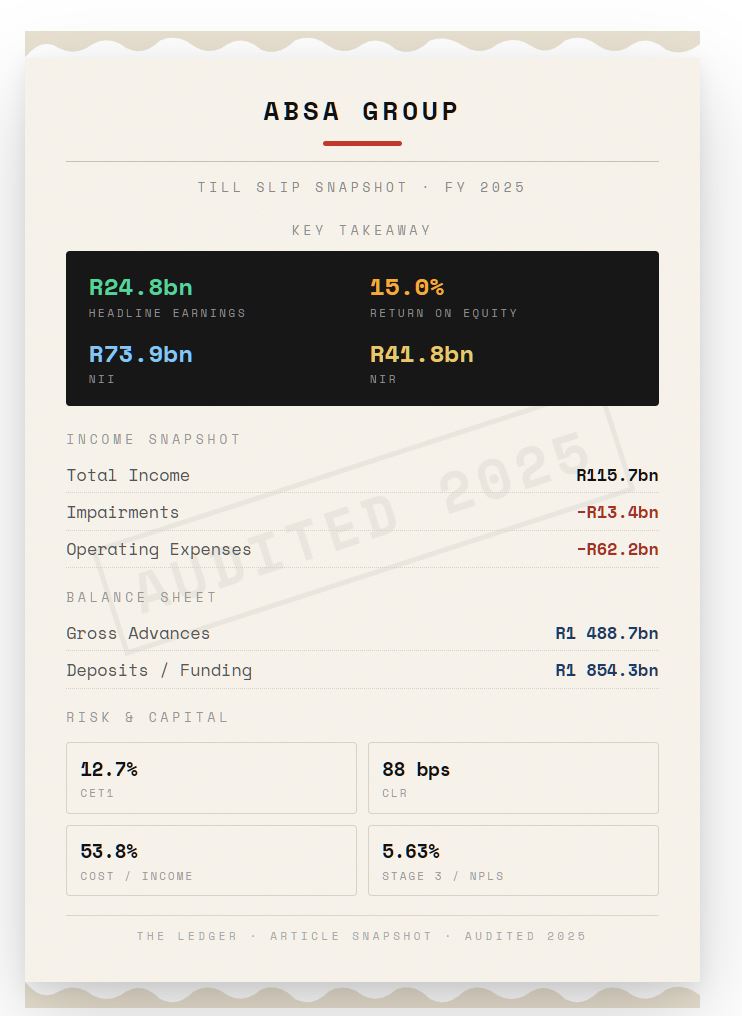

- Absa reported headline earnings of R24.8 billion, up 12%, with ROE at 15.0% and a CET1 ratio of 12.7%.

- The real earnings engine sat inside Corporate and Investment Banking, which generated R13.0 billion in headline earnings and roughly 48% of group profits.

- Africa Regions contributed 31% of group earnings, while weighted GDP growth across those markets sat around 4.8%, well above South Africa.

- The deeper question is whether South African banks are increasingly using domestic balance-sheet strength and capital-market depth to fund growth across the continent.

South Africa’s economy continues to grow slowly. Yet its largest banks remain profitable, well-capitalised and capable of producing respectable returns.

Absa’s FY25 results offer an explanation. The group delivered headline earnings of R24.8 billion, up 12%, while revenue rose 5% to R116 billion and return on equity edged up to 15.0%. On the surface, this looks like a familiar bank-results story: decent growth, stable capital, manageable impairments.

But the more interesting story sits underneath the headline line. The results suggest a bank that is gradually earning its growth from a broader geographic and strategic base — one where corporate banking, capital markets and African operations are doing more of the heavy lifting than the traditional South African retail franchise.

In that sense, Absa’s latest numbers are not just about a better year. They may be pointing to a different model of South African banking altogether.

The investment bank inside Absa

The clearest strategic signal in the results is the growing weight of Corporate and Investment Banking. CIB generated R13.0 billion in headline earnings in FY25 and accounted for roughly 48% of group profits. Its total income rose 9%, helped by a 16% increase in non-interest income.

That matters because it changes the nature of the earnings story. This is not simply a bank lending more money into a weak domestic economy. Much of the momentum came from activities like trading, markets, corporate banking and capital-markets intermediation — businesses that generate revenue from the movement of money, not just the price of money.

The composition of that growth is telling. Global Markets revenue broadened across desks, particularly in fixed income, currencies and commodities. These are the businesses that sit close to cross-border trade, funding, hedging and large corporate transactions. Absa also reported R35 billion in sustainable financing through CIB, with the group total at R53 billion.

In other words, the rise in CIB earnings is not just a volume story. It points to a strategic tilt toward the kinds of businesses that benefit when companies trade across borders, raise capital, hedge exposures or finance larger projects. The deeper implication is that Absa is increasingly behaving like a regional financial intermediary, not merely a South African lender with offshore branches.

| CIB signal | FY25 | Why it matters |

|---|---|---|

| Headline earnings | R13.0bn | CIB is now one of the main profit engines of the group. |

| Total income growth | +9% | Growth was broad enough to matter at group level. |

| Non-interest income growth | +16% | Signals more platform-like earnings, less dependent on plain lending spreads. |

| Credit loss ratio | 0.21% | Strong profitability arrived without a deterioration in credit quality. |

Retail is no longer the whole story

None of this means retail banking no longer matters. It means its role appears to be changing.

Absa’s Personal and Private Banking division delivered R7.5 billion in headline earnings. Revenue grew a modest 2%, while digitally active customers increased 4%, products per customer rose to 2.7, and transactional deposits grew 11%. The numbers do not suggest a roaring retail growth story. They suggest something subtler: repair.

Asset quality improved across much of the retail book. The PPB credit loss ratio declined from 1.89% to 1.69%. In home loans it moved from 0.39% to 0.34%; in vehicle and asset finance from 1.62% to 1.26%. These are not flashy numbers, but they matter because they show a retail franchise regaining balance.

Retail, then, looks less like the primary source of momentum and more like the part of the bank that provides stability: deposits, customer engagement, and improving asset quality. That matters in a group where other divisions are taking on the heavier growth burden.

Retail appears to be doing a different job now: less spectacular growth, more balance-sheet stability.

The balance sheet is growing, but carefully

Another striking feature of Absa’s FY25 results is what did not happen. There was no aggressive balance-sheet surge.

Net customer loans rose 6% to R1.35 trillion, while customer deposits increased 6% to R1.44 trillion. The group’s Common Equity Tier 1 ratio remained strong at 12.7%, slightly above the top end of its board target range. The bank is clearly still growing, but it is doing so with discipline.

The quality of growth also improved. Group credit impairments fell, helping the credit loss ratio decline to 0.88%, down from 1.03% the previous year and back into the target range of 75 to 100 basis points. Stage 2 coverage improved from 5.98% to 5.30%, while Stage 3 coverage moved down from 47.4% to 45.8%.

This is important because it suggests the earnings improvement was not the result of stretching the balance sheet for growth. It came with stable capital, better impairments and a reasonably measured expansion in lending. That is usually a sign of management trying to improve the economics of the franchise rather than merely enlarging it.

The African growth equation

The geographic pattern in the results may be the most revealing signal of all.

Absa’s presentation notes that weighted GDP growth across its Africa Regions was around 4.8%, versus a much weaker domestic backdrop. At the same time, Africa Regions contributed 31% of group earnings. In the Africa retail and business banking segment, headline earnings climbed from R1.7 billion to R2.5 billion, while return on equity jumped from 12.1% to 17.1%.

The business also reported 14% growth in revenue, 14% growth in active customers to 3.0 million, and customer loan growth of 10% in constant currency. These are not side notes in the pack. They are evidence that a meaningful part of group momentum is now coming from faster-growing markets outside South Africa.

Once you read the results through that lens, the strategy starts to cohere. South Africa still offers the deepest capital markets, strongest institutional funding base and most sophisticated financial system on the continent. But it does not offer the strongest growth. The rest of Africa, by contrast, offers exactly that — though with more volatility. The combination suggests a model in which South African banking platforms provide stability and funding depth, while regional operations provide incremental growth.

If South Africa provides the plumbing, the rest of Africa increasingly provides the growth pressure running through it.

The funding signal nobody should ignore

There is another, quieter story in the results, and it sits in the net interest margin bridge.

Absa disclosed that deposit pricing reduced the net interest margin by 16 basis points. That is a useful clue. It suggests deposits are becoming more competitive and more expensive. In other words, funding is becoming a strategic battleground.

This matters because banks do not expand into higher-growth markets on strategy slides alone. They do so with funding. If domestic deposit competition intensifies, banks with access to deeper capital markets gain an advantage. South Africa still has one of the continent’s deepest pools of institutional capital — pension money, insurance balance sheets, asset managers and debt markets that many other African systems simply do not match.

That raises a wider question, one Absa’s numbers only begin to hint at: are South African banks increasingly using domestic balance-sheet strength and capital-market depth to finance activity elsewhere on the continent?

If so, the real story is bigger than Absa. It is about whether South African banks are evolving into continental capital intermediaries — raising, allocating and pricing money across a broader African system.

Banking beyond South Africa

Taken together, Absa’s FY25 results suggest a bank in strategic transition.

CIB is doing more of the earnings work. Retail is stabilising and improving the quality of the deposit and credit base. The balance sheet is growing, but with discipline. Africa Regions are contributing a meaningful and growing share of profits. And funding dynamics are starting to hint at a deeper contest over who gets to deploy capital across the continent.

That makes this more than a results story. It is a strategic one.

Absa may still be seen by many readers as a South African bank first. But its latest numbers suggest the next chapter of profitability may be increasingly shaped by what happens beyond South Africa’s borders — in capital markets, in cross-border corporate activity, and in the faster-growing economies north of the Limpopo.

The future of South African banking, in other words, may be becoming less domestic than its nameplates still imply.

The Ledger View

- Main signal: Absa’s strongest momentum is increasingly coming from the parts of the bank closest to cross-border money flows, not just domestic retail lending.

- Strategic shape: Retail looks like the stabiliser; CIB and Africa look like the growth optionality.

- Funding question: Deposit competition matters because continental expansion ultimately depends on who controls cheap and scalable funding.

- Bigger implication: Absa’s results hint at a future in which South African banks become regional allocators of capital, not only domestic intermediaries.