- Cocoa prices briefly surged above $12,000 per tonne during the 2024 shock.

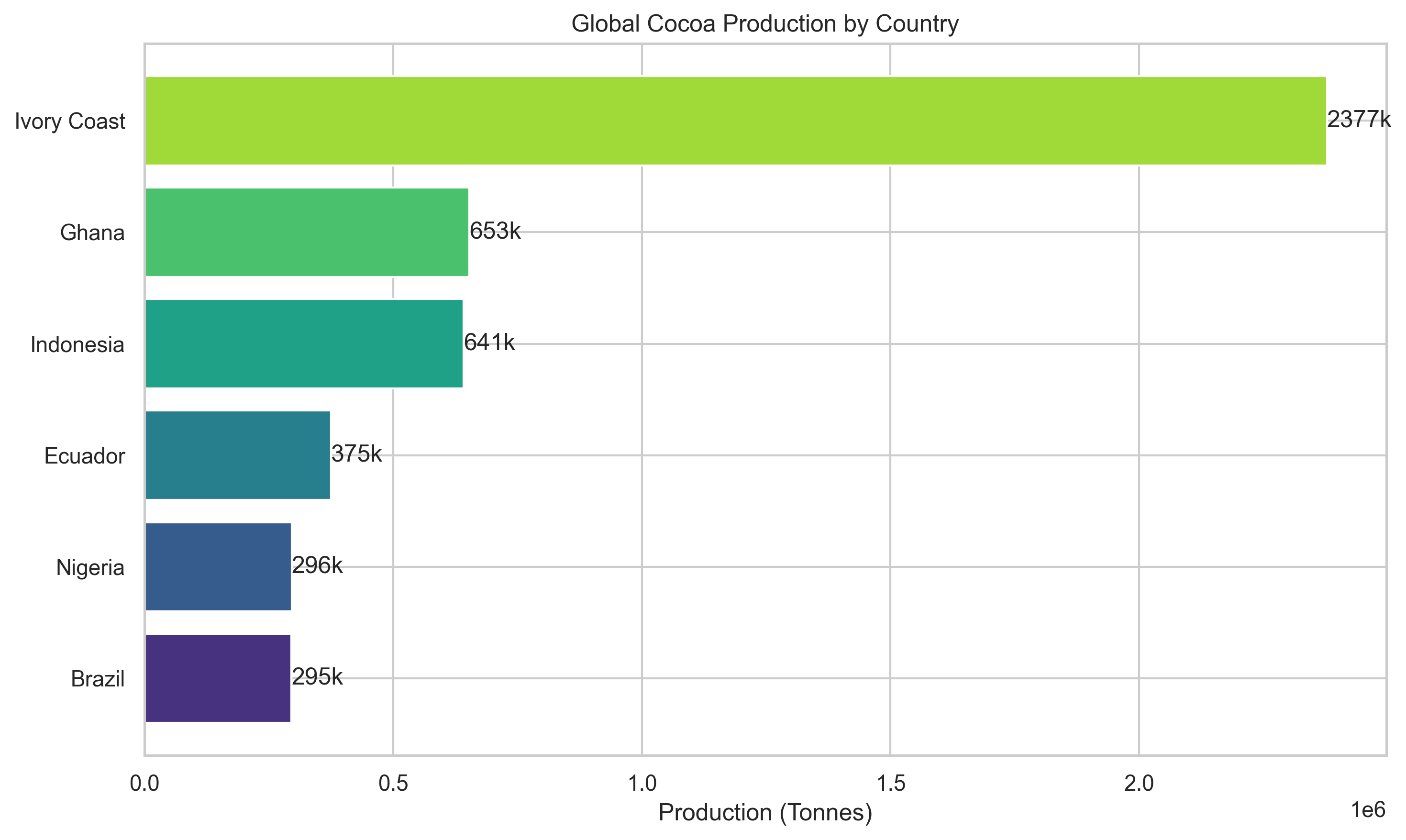

- West Africa produces most of the world's cocoa, but captures only a small share of the final value chain.

- The supply crisis was not a one-off weather event; it reflected ageing trees, disease pressure, climate volatility and underinvestment.

- The deeper lesson for agri-finance is that biological production cycles and financial markets now move at very different speeds.

In early 2024 the global commodities market witnessed what traders would later describe as a once-in-a-generation shock. While much of the post-pandemic world was celebrating cooling inflation, cocoa futures were doing something extraordinary: they were going vertical.

Within months prices surged past $12,000 per metric tonne, roughly four times their historical average. On global commodity exchanges, cocoa briefly became the best-performing major agricultural commodity in the world.

For a moment the global chocolate industry appeared to be facing its own version of the 1970s oil crisis.

Yet two years later the landscape looks very different. Farmers in Côte d’Ivoire and Ghana—countries responsible for roughly two-thirds of global cocoa production—have not experienced the windfall that many observers expected.

Instead the industry finds itself caught in a classic value-chain paradox: the price of the commodity surged, but most of the profits flowed elsewhere.

The Price Shock

For more than a decade cocoa prices fluctuated within a relatively stable range between $2,000 and $3,500 per tonne. Then in 2024 a combination of extreme weather, crop disease and speculative market activity triggered an unprecedented supply shock.

The spike was dramatic but temporary. As supply chains adjusted and demand softened, prices retreated sharply. By early 2026 cocoa futures had fallen back toward more historically recognisable levels.

But commodity markets do not leave these episodes unchanged. A price shock of this magnitude alters purchasing behaviour, hedging decisions, formulation choices and long-term investment plans across the entire value chain.

Commodity booms do not automatically become farmer booms.

The Structural Supply Problem

The cocoa crisis did not emerge from a single failed harvest. It reflected a sector that had already been weakening beneath the surface.

The first problem is biological. A large share of cocoa tree stock across West Africa is ageing. Older trees produce lower yields, are less resilient to heat and rainfall volatility, and are more vulnerable to disease. Replanting is expensive, takes years to restore productivity and often requires smallholders to absorb a period of lower cash flow before benefits materialise.

The second problem is phytosanitary. Disease pressures, including swollen shoot and other productivity-reducing infections, have steadily eroded yields in key growing areas. For smallholder producers, diseased trees are not simply a crop issue; they are a balance-sheet issue.

The third problem is economic. Fertiliser, labour and fuel costs rose sharply after the global inflation shock, making it harder for farmers to maintain orchards properly. In practice, underinvestment in tree rehabilitation today becomes lower output tomorrow.

The 2024 price spike, then, was less a bolt from the blue than the visible market expression of a long-building production problem.

The Colonial Blueprint of Cocoa

To understand why West Africa captures so little of the cocoa industry's profits, one must look beyond the price charts.

The modern cocoa supply chain still reflects an economic architecture designed during the colonial era. West African territories were positioned primarily as producers of raw beans, while the industrial stages of grinding, refining, branding and distribution remained concentrated in Europe.

Grinding—the process that converts beans into cocoa liquor, butter and powder—requires expensive machinery, industrial energy inputs and access to downstream manufacturing networks. Those capabilities historically accumulated outside the producing regions.

The imbalance is clear. Côte d’Ivoire alone produces more than two million tonnes of cocoa each year, while neighbouring Ghana produces hundreds of thousands more. Together the two countries dominate global supply.

Yet the highest value segments of the industry—processing, branding, formulation and retail—remain largely outside the region. This is why production dominance does not automatically translate into profit dominance.

The Pricing Paradox

At first glance the cocoa boom should have delivered a windfall to farmers. But global cocoa markets do not operate as a simple pass-through system from futures prices to farm income.

In both Ghana and Côte d’Ivoire, large parts of the crop are marketed through institutional structures that aim to stabilise farmer incomes by setting farm-gate prices in advance. This helps protect smallholders during price collapses, but it also means they do not necessarily participate fully when prices spike violently.

In effect, the 2024 boom occurred faster than the physical crop-pricing system could adjust. By the time international prices had exploded, a significant portion of the commercial structure had already been set on earlier assumptions.

This is the real paradox of the cocoa surge: the gains were most visible in the financial layer of the market, while the physical farm economy adjusted only partially and with a lag.

The Great Substitution

Economics teaches a simple lesson: when a commodity becomes too expensive, markets find ways to use less of it.

Facing record cocoa prices in 2024, major chocolate manufacturers began experimenting more aggressively with alternative formulations. Food scientists increasingly turned to Cocoa Butter Alternatives (CBAs)—vegetable fats derived from palm, shea and other tropical oils that can mimic some of the functional characteristics of cocoa butter.

These substitutes do not eliminate cocoa from chocolate, but they can reduce intensity at the margin. And once manufacturers discover formulations that preserve taste, shelf stability and margins, they have little incentive to return fully to the old recipe.

For cocoa-producing countries, that matters. A price spike can destroy demand at the margin even as it raises revenues temporarily. High prices may therefore contain the seeds of future weakness.

The Margin Squeeze

Another reason farmers missed the boom lies in the timing mismatch between output prices and input costs.

Farm-gate systems cushioned farmers from collapse, but they could not shield them from rising operating costs. Fertiliser remained expensive. Labour costs remained elevated. Transport and fuel costs did not reset as quickly as international commodity prices.

During the 2024 spike, farmers were effectively trapped between two systems moving at different speeds: a global futures market that repriced instantly, and a local production economy that repriced slowly while input inflation persisted.

That is what a true margin squeeze looks like in agriculture: not simply low prices, but weak income transmission combined with sticky costs.

Where the Money Really Goes

Perhaps the most revealing insight into the cocoa economy comes from examining how the value of a chocolate bar is distributed.

Farmers typically capture only a small fraction of the final retail value. Manufacturing, branding, packaging, distribution and retail capture the majority.

In other words, although West Africa produces most of the world’s cocoa, the largest profits emerge further down the supply chain. This is not a temporary distortion. It is the defining structure of the industry.

The Strategic Shift: Owning the Grind

Recognising this imbalance, governments in Ghana and Côte d’Ivoire have periodically argued for more domestic processing. The logic is straightforward: if the continent cannot capture enough value at the bean stage, it must move into the industrial stages that follow.

By converting beans into cocoa butter, liquor and powder locally, producing countries can retain more of the economics embedded in chocolate before the product enters global manufacturing chains.

Such a shift would also create downstream employment in logistics, engineering, manufacturing and quality control—industries that historically developed outside Africa.

The challenge, however, is that processing alone is not enough. Competitiveness still depends on reliable power, logistics, access to capital, technical capability and stable policy support. Value capture is an industrial strategy, not merely a slogan.

The Deeper Risk for Agricultural Finance

For lenders, investors and agricultural policymakers, the cocoa episode points to a broader risk in global commodity markets.

Biological production systems move slowly. Trees take years to mature. Disease control takes seasons. Climate damage is not repaired in a quarter. But financial markets reprice instantly.

The gap between these two speeds—biological production and financial pricing—is widening.

That matters for agri-finance. Credit models, working-capital assumptions and portfolio monitoring frameworks cannot rely only on spot-price signals. They must also account for supply biology, input affordability, disease pressure and the lag with which global prices filter through to farm cash flow.

In that sense, the cocoa boom was not merely a commodity story. It was a reminder that agricultural risk is increasingly shaped by the interaction between climate, biology, market structure and finance.

The Ledger View

- Commodity paradox: record cocoa prices did not translate into proportionate farmer prosperity.

- Structural imbalance: West Africa dominates production, but not value capture.

- Demand risk: substitution may permanently reduce cocoa intensity in mass-market chocolate.

- Finance lesson: agricultural credit risk must account for the widening gap between biological production cycles and financial market pricing.