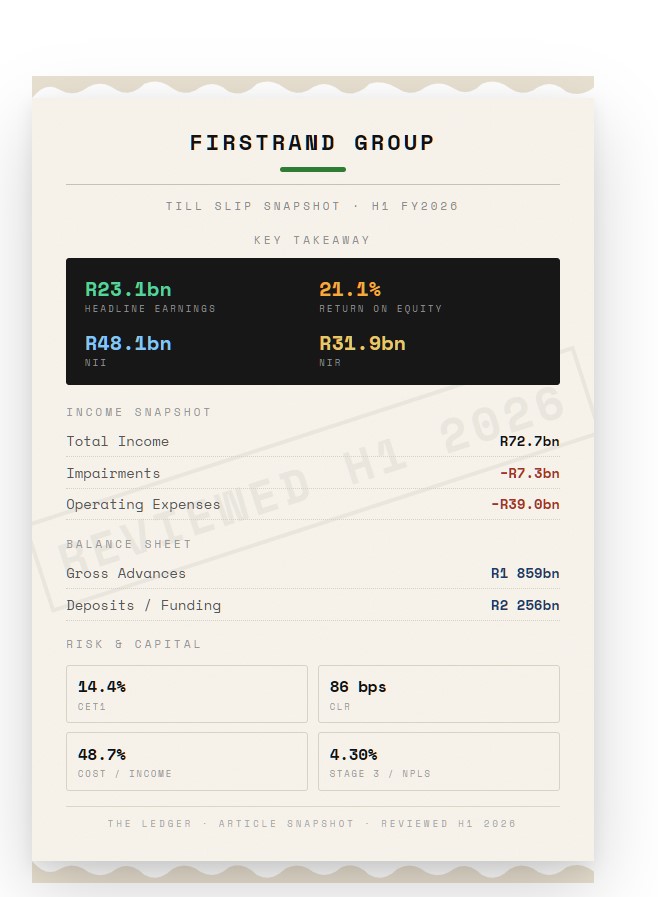

- FirstRand reported normalised earnings of R23.2 billion and ROE of 21.1% in a weak-growth environment.

- Non-interest revenue rose 12% to R31.9 billion, growing faster than net interest income.

- The bank’s impairment charge was R7.34 billion, while the credit loss ratio remained contained at 0.86%.

- The deeper question is whether South Africa’s major banks are becoming increasingly decoupled from the macroeconomic realities below them.

There is an interesting dichotomy at the heart of South Africa’s financial system.

On the ground, the economy continues to struggle to get enough runway to take flight. Economic growth remains subdued, infrastructure bottlenecks persist, and household balance sheets are still adjusting after one of the sharpest interest-rate cycles in recent memory.

Yet several thousand metres above this landscape, the country’s Big Four banks appear to be operating in a very different atmosphere.

For the six months ended December 2025, FirstRand reported normalised earnings of R23.2 billion, an increase of 11% year-on-year, alongside a return on equity of 21.1%.

In global banking terms these are elite numbers. In a domestic economy growing at barely one percent, they are extraordinary.

The result is a growing sense that South Africa’s banking sector, particularly the Big Four, operates at what might be described as high altitude. From that vantage point the turbulence of the real economy is still visible, but the cabin remains pressurised.

Understanding how this happens requires looking beyond headline profits and examining the structure of modern banking income.

Profitable Banks in a Low-Growth Economy

South Africa’s macroeconomic backdrop remains fragile.

Economic growth has struggled to break through the two-percent ceiling for most of the past decade. Structural constraints in electricity, logistics and public infrastructure continue to weigh on productivity and investment.

For households, the consequences are visible in slow income growth (wages) and elevated debt burdens. Millions of consumers remain financially stretched after the recent tightening cycle that started in late 2022.

Against this backdrop, the financial sector’s profitability appears almost detached from the broader South African economy.

But the explanation is less mysterious than it first appears.

Banks have gradually transformed their business models. Lending is no longer the sole engine of profitability. Instead, banks increasingly generate earnings through platform-based financial ecosystems, combining transactional services, insurance products, investment management and advisory activity.

The result is an institution capable of producing robust returns even when economic growth remains weak.

The banks are flying. The economy is still on the runway.

The Recipe of the R23 Billion

FirstRand’s interim results illustrate this shift clearly.

Total group income is now driven by three core components:

• Net interest income (NII)

• Non-interest revenue (NIR)

• Credit impairments

During the six-month period, net interest income rose 8% to R48.1 billion, supported by disciplined lending growth and the continued strength of the group’s deposit franchise.

But the more interesting story lies elsewhere.

Non-interest revenue grew even faster, rising 12% to R31.9 billion.

This category includes transaction fees, insurance income, advisory services, asset management fees and a growing range of platform-based financial services.

In other words, a substantial portion of modern banking profits now comes not from lending money, but from facilitating the movement and management of money.

| Metric | H1 FY2026 | Commentary |

|---|---|---|

| Normalised Earnings | R23.2bn | Strong profitability in a subdued macro environment. |

| ROE | 21.1% | Still among the strongest return profiles in South African banking. |

| NII | R48.1bn | Core earnings engine remains strong. |

| NIR | R31.9bn | Fast-growing fee and platform income becoming more strategically important. |

| Impairments | R7.34bn | Up 6% year-on-year, but still contained relative to the size of the book. |

| Credit Loss Ratio | 0.86% | Credit quality remains resilient rather than distressed. |

| Stage 3 Loans | 4.30% | Broadly stable, suggesting stress without crisis. |

Managing the Balance Sheet - Net Interest Income

Despite the rise of fee-based revenue, net interest income remains the backbone of banking profitability.

The challenge for banks during the current cycle has been navigating the transition from rising interest rates to a potential easing environment.

Normally, falling interest rates compress margins by reducing the spread between lending rates and funding costs. Yet FirstRand managed to grow interest income even as the cycle began to turn.

The key lies in treasury and asset-liability management.

Through careful balance-sheet positioning, the group’s treasury function actively manages the duration and repricing profile of assets and liabilities. This allows the bank to mitigate the impact of interest-rate movements and protect margins.

The Rise of Non-Interest Revenue

If net interest income represents the structural foundation of banking profitability, non-interest revenue is increasingly the growth engine.

The reason is simple: fee-based income is less capital-intensive and less sensitive to credit risk.

Within FirstRand, this shift is most visible in the performance of FNB’s digital banking ecosystem.

Millions of customers now interact with the bank’s digital platforms each month, conducting payments, managing savings, purchasing insurance products and accessing financial services through the mobile app.

Each of these interactions generates incremental revenue.

Rather than simply monetising credit risk, the institution monetises financial activity itself.

Credit Quality- Stress Without Crisis

The group reported an impairment charge of R7.34 billion, representing a 6% increase year-on-year, while the credit loss ratio remained contained at 0.86% of advances.

Stage 3 loans, the banking system’s measure of non-performing credit, stood at 4.30% of total advances, broadly stable relative to previous periods.

These figures suggest that while financial stress is present, the credit cycle has remained manageable.

For now, the pain on the ground has not fully translated into panic in the balance sheet.

The Banking Paradox

Why does the financial sector continue to generate world-class returns while the broader economy struggles to grow?

Part of the answer lies in market structure. South Africa’s banking sector is highly concentrated, with significant barriers to entry and strong pricing power.

But the more interesting explanation lies in the changing nature of banking itself.

As transaction services, digital platforms and fee-based income become increasingly important, bank profitability becomes less tightly linked to economic growth.

In effect, banks can increasingly grow within the economy rather than alongside it.

The Passengers Who Ordered the Meal

Behind every banking result lies a far broader economic story.

The same economy that produces R23 billion in banking profits is also the economy in which millions of households carefully balance monthly budgets.

For many South Africans, the financial system is experienced through loan repayments, debit orders and interest charges rather than dividend declarations.

Banks remain essential institutions, financing businesses, enabling investment and providing the infrastructure that allows modern economies to function.

But the contrast between financial sector profitability and everyday economic experience remains striking.

From thirty thousand feet the landscape can look orderly and predictable.

On the ground, the terrain is far more complex, this is something we have to continue to grapple with in a developmental state.

Cruising Altitude

FirstRand’s interim results ultimately illustrate the evolution of the modern banking institution.

Through diversified franchises, strong deposit franchises, disciplined credit management and sophisticated balance-sheet strategies, the group has built an institution capable of generating consistent returns even in a low-growth environment.

At 21.1% return on equity, the bank continues to operate comfortably above the cost of capital.

In aviation terms, the aircraft has reached cruising altitude.

The turbulence of the real economy is still visible below.

But inside the cabin, the air remains remarkably calm.

And for now at least, South Africa’s largest banks continue to dine comfortably in the sky.

The Ledger View

- Earnings engine: FirstRand’s profitability is increasingly supported by a mix of NII strength and structurally rising NIR.

- Credit takeaway: Impairments remain elevated enough to matter, but contained enough to preserve confidence in the book.

- Strategic implication: Large South African banks are becoming more insulated from weak macro growth through platform economics and balance-sheet discipline.

- Bigger question: Banking resilience is good for shareholders, but the widening gap between bank outcomes and economic outcomes is becoming harder to ignore.