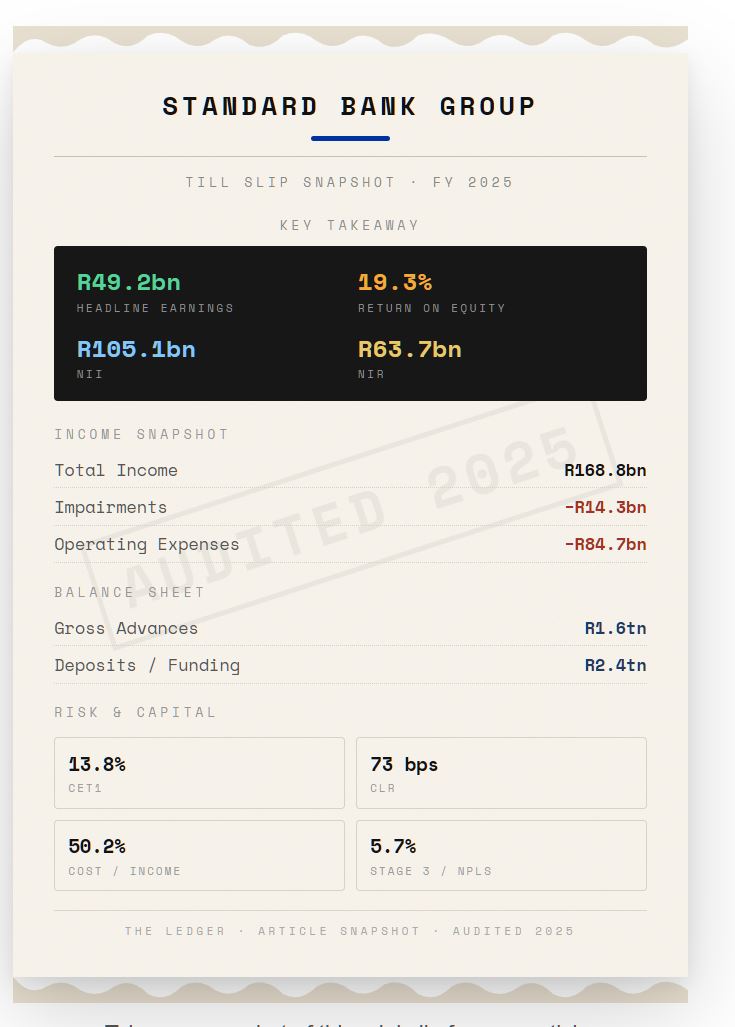

- Standard Bank reported headline earnings of R49.2 billion and ROE of 19.3%, with the economics of its pan-African network beginning to show.

- Non-interest income is increasingly doing the heavy lifting, with fees and trading income growing faster than the traditional lending engine.

- The group’s cost-to-income ratio improved to 50.2% while the credit loss ratio fell to 73bps, suggesting scale and discipline are arriving together.

- The deeper question is whether Standard Bank is no longer just a lender, but increasingly Africa’s financial railway for money.

In 1989, a small private rail company in Pretoria began restoring old locomotives and carriages from the early twentieth century. The result was Rovos Rail, now widely regarded as one of the most luxurious train journeys in the world.

Its flagship route runs from Cape Town to Dar es Salaam, covering nearly 6,000 kilometres across six African countries. The journey takes more than two weeks.

But the real lesson is not about tourism.

Railways work because they connect places and people that previously operated in isolation. Once the rails exist, trade flows more easily, goods move further and economic activity expands along the route.

Financial networks behave in much the same way.

Standard Bank’s latest results suggest that the most valuable infrastructure on the continent right now may increasingly be the financial rails connecting its many diverse economies.

Many geographies, many headaches

For years, Standard Bank’s strategy looked complicated.

While many global banks retreated into their domestic markets after the global financial crisis, Standard Bank quietly expanded across the African continent, building operations in more than 20 markets and linking them through global financial hubs in London, Dubai, New York and Beijing.

To investors, the model often appeared messy.

Different currencies. Different regulators. Different political risks.

Yet financial networks, much like railways, telecom cables or power grids — only reveal their true economic potential once they reach sufficient scale.

Standard Bank’s latest results suggest that moment may finally be arriving.

The group reported headline earnings of R49.2 billion, up 11%, and a return on equity of roughly 19%, placing it among the most profitable large banks in emerging markets. More interesting than the numbers themselves, however, is what is driving them: a growing share of revenue now comes not from lending, but from the financial activity flowing across the bank’s continental network.

| Metric | FY2025 | Read-through |

|---|---|---|

| Headline Earnings | R49.2bn | The clearest evidence yet that the long continental strategy is monetising at scale. |

| ROE | 19.3% | Still a very strong return profile for a bank operating across volatile jurisdictions. |

| Cost-to-Income | 50.2% | Suggests scale economies and cost discipline are finally converging. |

| Credit Loss Ratio | 73bps | Credit quality improved rather than deteriorated, despite a complex operating backdrop. |

| CET1 Ratio | 13.8% | Capital remains robust enough to support growth, resilience and distributions. |

Building the Financial Rails of a Continent

For decades African finance has been fragmented.

Colonial banking systems produced national financial silos, and cross-border trade between African countries was often financed through banks headquartered outside the continent. The result was a curious imbalance: Africa needed infrastructure — roads, ports, power plants — yet the financial rails connecting its economies remained underdeveloped.

Standard Bank’s strategy was to build those rails.

Operating across much of the continent, the bank positioned itself at the intersection of trade finance, commodity flows, infrastructure funding and cross-border capital movement. This positioning is particularly valuable in an economy defined by resources and trade: commodities produced in Zambia or Angola, processed in South Africa, and exported to Asia all require financing, hedging and settlement.

Banks facilitate that activity and when a bank sits in the middle of the network, it begins to resemble something closer to infrastructure than a traditional lender. This matters when viewed through the lens of demographics. Africa is expected to account for a large share of global population growth over the coming decades and already has the youngest population in the world. Rising urbanisation, trade and financial inclusion will require payment systems, credit markets and capital flows to expand dramatically.

A bank that already operates across those markets effectively owns a portion of the continent’s financial plumbing.

If controlled well, such a network can become extremely profitable.

Once enough track has been laid, the network itself becomes the moat.

The Demographic dividend

Africa is expected to account for a significant share of global population growth in the coming decades and already has the youngest population in the world.

More people. More urbanisation. More trade. More financial activity.

All of this requires payment systems, capital markets and credit infrastructure. A bank already embedded across these economies effectively owns part of the continent’s financial plumbing.

The Quiet Rise of Non-Interest Income in Banking

Perhaps the most interesting feature of Standard Bank’s results is the source of its growth.

Net interest income, the traditional engine of banking, grew only modestly, rising around 4%. By contrast, fee and commission income increased roughly 11% while trading revenue rose about 10%.

This reflects a structural shift in the economics of banking.

Historically, banks made money primarily by borrowing short and lending long — collecting interest margins on loans.

But the most profitable banks increasingly operate as financial platforms.

Payments.

Foreign exchange.

Trade finance.

Capital markets.

These activities generate revenue without requiring large additions to the balance sheet.

The distinction is important.

Lending consumes capital.

Transactions consume networks.

Standard Bank has spent two decades building exactly that network across the continent.

South Africa for efficiency, Africa for growth

The geographic structure of Standard Bank’s franchise also explains much of the bank’s resilience.

South Africa remains the most sophisticated financial market on the continent, offering deep capital markets, institutional investors and regulatory stability. It provides the efficiency and operational scale that large banks require.

But growth increasingly comes from elsewhere.

Many African economies continue to expand significantly faster than South Africa while remaining under-banked. Rising trade flows, infrastructure investment and financial inclusion are gradually expanding the addressable market for banking services across the continent.

For Standard Bank, this creates a useful balance.

South Africa provides stability and efficiency.

The rest of Africa provides growth.

The combination helps smooth the volatility that historically characterised African banking.

Volatility Can Be Profitable

Another interesting feature of the results is the strength of trading revenue.

Currency volatility, commodity price swings and shifting interest-rate expectations often create uncertainty for businesses operating across African markets. Exporters hedge currency exposure. Importers manage payment risk. Investors adjust portfolios.

Banks sit in the middle of those transactions.

In calm markets banks lend money.

In volatile markets they sell protection against uncertainty.

For a bank deeply involved in commodity-linked African economies, that volatility can translate into steady revenue through trading desks and hedging products.

The Global Markets division delivered strong growth on the back of these contradictions.

Credit Quality Quietly Improving

Despite relatively weak economic growth in parts of the continent, Standard Bank’s credit metrics improved during the year, with the credit loss ratio declining to roughly 73 basis points from around 83 basis points previously.

Part of this reflects stabilising economic conditions.

But another part reflects the evolution of credit analytics within modern banks. Behavioural scoring, early warning systems and real-time monitoring increasingly allow lenders to detect distress well before borrowers default.

Collections start earlier.

Restructuring happens sooner.

Defaults are sometimes prevented entirely.

In credit markets, the most valuable signal is rarely who has already defaulted.

It is who might default next.

The bank may increasingly be earning more from the movement of money than from the price of money.

The network effect in banking

The surprising takeaway from Standard Bank’s results is that the bank may increasingly earn money not by lending more, but by facilitating more transactions.

Infrastructure companies earn money by charging tolls. Financial networks do something similar — they earn fees each time money moves through the system.

The broader lesson from Standard Bank’s results is that scale across financial networks matters.

Physical infrastructure — roads, railways and ports — allows goods to move across an economy.

Financial infrastructure allows capital to move.

Banks capable of connecting multiple economies, financing trade, managing currency risk and funding infrastructure effectively become part of that infrastructure themselves.

For years, Standard Bank’s pan-African strategy appeared complicated and expensive.

Now the economics of the network are beginning to reveal themselves.

Diversified income streams.

Expanding transactional activity.

Improving credit performance.

And scale across jurisdictions.

The bank once described itself simply as “Africa’s bank.”

Its results increasingly suggest something slightly different.

Standard Bank may be becoming Africa’s financial railway for money.

The Ledger View

- Strategic payoff: The continental footprint is no longer just a complexity story. It is increasingly a scale and network-effects story.

- Earnings engine: The growth mix matters. Non-interest income is doing more of the work, which makes the franchise more platform-like and less balance-sheet dependent.

- Credit takeaway: Falling impairments alongside resilient capital suggest control has improved even as the geographic footprint remains wide.

- Bigger question: If Standard Bank becomes the financial rails of African commerce, the long game may prove more profitable than most investors once assumed.