- South Africa’s CEO pay debate is not only about whether executives are overpaid, but whether firms can keep concentrating reward at the top while the wage base beneath them remains too weak to support a more inclusive economy.

- In the JSE-listed wholesale and retail sector, Just Share reported an average unweighted ratio of 597x between CEO pay and the total remuneration of the lowest earner, with the highest ratio reaching 1,308x.

- The deeper argument is that executive pay can be lifted by two winds at once: weak bargaining systems below and macroeconomic windfalls above.

- South Africa’s most interesting alternative route may not have been payroll at all, but broad-based ownership structures such as Phuthuma Nathi.

Henry Ford is often remembered for a simple but powerful insight: a company cannot build a mass market on wages too low for its own workers to participate in it. By paying workers enough to become consumers of the economy they helped power, Ford did more than solve a labor problem. He helped show that wages were not only a cost to be squeezed, but part of the demand base that kept industry alive. Modern executive pay often runs in the opposite direction. In South Africa, the question is no longer whether firms use profits to reward success. It is whether too much of that reward is extracted at the top, while the wage base beneath it remains too weak to sustain a more balanced form of capitalism.

South Africa’s CEO pay debate is not just about whether executives are overpaid. It is about whether firms can keep concentrating reward at the top while the wage base beneath them remains too weak to support a more inclusive economy. Executives are often rewarded on near-global terms, while the workers who help create that value are paid within a weak local wage structure. In that system, pay at the top reflects not only performance, but power: the ability to claim a disproportionate share of value because bargaining systems below are too weak to resist it. In cyclical sectors, macroeconomic windfalls can lift executive rewards even further through commodity booms, asset re-ratings and market tailwinds. The usual defense is that top executives are scarce and carry enormous responsibility. Sometimes that is true. But in a highly unequal economy, large pay packets can also reveal who has the strongest power to extract value inside the firm. The real question is whether thousands can create value collectively while the rewards flow as if only a few at the top truly produced it.

What CEO Pay Ratios Really Measure

CEO-worker pay ratios matter because they make inequality visible. But they also reveal something more uncomfortable than executive excess: they show how little bargaining power exists further down the organisation. Just Share’s work on JSE-listed companies has shown that South African vertical pay-gap disclosure remains inconsistent and incomplete. Even so, where firms do disclose, the gaps are often startling. In the JSE-listed wholesale and retail sector, Just Share reported an average unweighted ratio of 597 between total CEO remuneration and the total remuneration of the lowest earner, with the highest ratio reaching 1,308.[3]

What does that mean in reality? If the lowest-paid employee earns R150,000 a year, a 597-times ratio implies the CEO earns R89.55 million a year. Spread across roughly 250 working days, that comes to about R358,200 per day. In other words, the CEO would earn more than that worker’s full annual pay before the first working week of the year is over. At 1,308 times, the distance becomes even more extreme: about R196.2 million a year, or roughly R784,800 per working day. That is not just a large gap. It is a different economic reality inside the same company. The ratio is not just measuring compensation. It is measuring power.[3]

The ratio is not just measuring compensation. It is measuring power.

What Actually Sits Inside a CEO Pay Packet

One reason these debates go nowhere is that many people imagine CEO pay as a single salary number. It rarely is. A typical package has three moving parts: fixed pay, short-term incentives and long-term incentives. Fixed pay is the guaranteed salary and benefits portion. Short-term incentives are annual bonuses tied to near-term targets such as earnings, return measures or operational milestones. Long-term incentives are usually share-linked awards that vest over several years and are meant to align executives with shareholder outcomes. Deloitte’s South African remuneration analysis and PwC’s JSE trends reporting both point to the growing importance of variable and long-term incentive structures in executive pay.[1, 2]

That distinction matters because the part of remuneration that really explodes is often not salary. It is the variable, market-sensitive layer. Workers are paid mainly in cash. Executives are increasingly paid in instruments that swell when earnings, valuations and market sentiment move in their favour. A CEO’s payslip is therefore only partly salary. The rest is a claim on performance, timing and market conditions.[1, 2]

How Weak Labor Systems and Boom Cycles Inflate CEO Pay

The standard defense of high CEO pay in emerging markets is scarcity. Boards argue that executives must navigate inflation, currency instability, political uncertainty, weak infrastructure, regulatory friction and volatile demand. In that context, higher executive pay is framed as rational retention policy rather than excess. That logic is not entirely wrong. But it is incomplete.[1]

In South Africa, executive pay can be lifted by two winds at once: weak bargaining systems below, which allow more value to be captured at the top, and macroeconomic windfalls above, which can swell earnings, valuations and incentive payouts beyond what individual effort alone would justify. The result is a system in which rewards at the top can rise much faster than the underlying distribution of value inside the firm would suggest. South Africa’s pay problem is not just that executives are rewarded globally while workers are paid locally. It is that the top can also be amplified by macro tailwinds that the rest of the wage structure never meaningfully shares.[1, 3]

Why Nordic Wage Gaps Are Smaller

This is where the Nordic comparison becomes useful. The Nordic model is not interesting because CEOs are saints or because hierarchy has disappeared. It is interesting because wage-setting institutions do more work across the whole labour market. In Sweden, collective bargaining coverage is above 90%; in Denmark and Finland it is around 80–90%; and in Norway it is roughly 60–70%. In South Africa, by contrast, the ILO’s latest country profile puts collective bargaining coverage at 30.1%. That difference matters. In the Nordics, the worker side of the pay ratio is lifted by stronger bargaining coverage, higher coordination and more normal wage compression before the remuneration committee ever meets. In South Africa, the structure is far weaker beneath the top, which makes it easier for executive pay to drift away from the wage base below.

That is why copying one or two Scandinavian governance ideas would miss the point. The real divide is institutional. In one system, labour markets shape the distribution beneath the top. In the other, the distribution below is weak enough that the top can float free from it. The OECD notes that bargaining coverage stays highest and most stable in systems with multi-employer agreements and strong employer organisation density — which is much closer to the Nordic model than the South African one.

South Africa’s Decade-Long Divergence

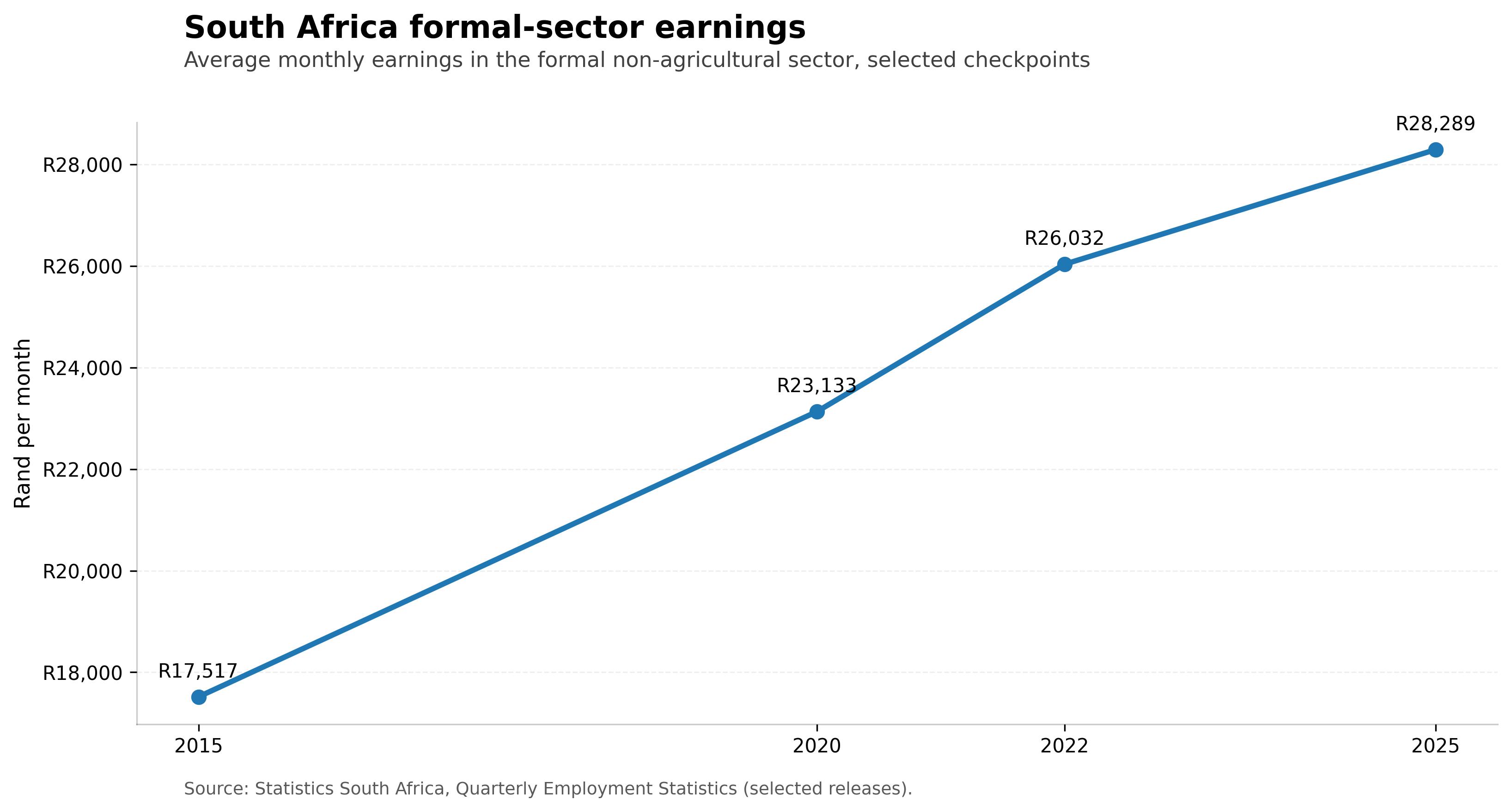

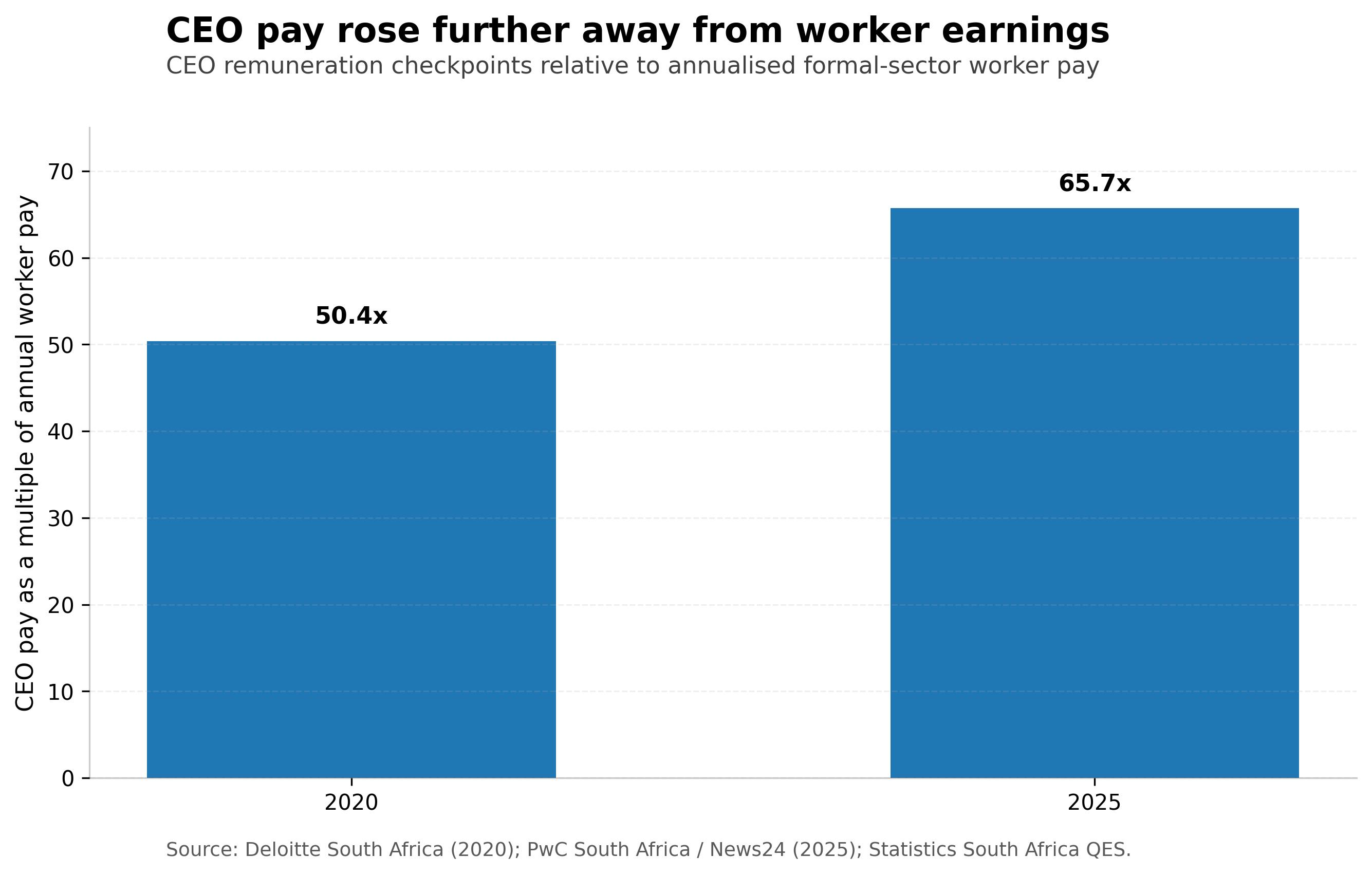

The data point in the same direction. On the worker side, Stats SA’s Quarterly Employment Statistics show average monthly earnings in the formal non-agricultural sector at R17,517 in November 2015 and R28,289 in February 2025.[5, 6] On the executive side, Deloitte reported that average total remuneration for CEOs across 250 surveyed companies was around R14 million in 2020, while PwC’s 2025 remuneration report said CEO total remuneration in its JSE Top 200 sample rose another 8%. News coverage of that PwC release put median CEO total remuneration at roughly R22.3 million.[1, 2, 7]

The important point is not simply that both lines rose. It is that they rose from radically different starting points and remained worlds apart. Worker earnings can improve over time and still do almost nothing to change the structure of inequality inside the firm. Once variable incentives and long-term awards are layered onto a low wage floor, even decent nominal earnings growth lower down leaves the underlying distance intact. South Africa’s pay debate is therefore not really about whether workers got raises. It is about whether the gains at the top moved so differently, and from such a higher base, that the ladder kept stretching anyway.[1, 5, 6]

How Commodity Booms Can Inflate CEO Pay

The cleanest place to see the distortion is in cyclical sectors such as mining and resources. A resource CEO can preside over rising earnings, stronger cash flow and a higher share price during a commodity upswing without necessarily extracting dramatically more physical output because of exceptional leadership alone. Commodity prices, external demand, exchange-rate moves and investor appetite can do much of the heavy lifting. Yet if remuneration is tied to shareholder returns, earnings growth or market-relative performance, the reward can still be enormous.[2]

This does not mean the CEO adds no value. It means executive pay often mixes managerial skill with macro tailwind and then reports the whole result as performance. In a commodity economy, remuneration committees can end up rewarding market beta as though it were managerial alpha. A rising share price can look like genius long before it proves anything of the sort. That is one reason executive incentives can feel so detached from the conditions facing workers. Workers live with inflation, weak bargaining power and slow wage progression. Executives can, at times, be carried upward by the cycle itself.[2]

South Africa Did Try Another Route

It would be unfair to say the country only tried to deal with inequality through wages. South Africa also experimented with broad-based ownership. That matters because ownership is a different route to participation in corporate upside. MultiChoice’s Phuthuma Nathi remains one of the clearest examples. MultiChoice says the scheme owns 25% of MultiChoice South Africa, has more than 73,000 black shareholders and has received R19.1 billion in dividends from MultiChoice South Africa since 2006. That is not symbolic language. It is a real example of broad-based participation in upside.[8]

The broader lesson is more sobering. Ownership models can be more transformative than wages, but only if they behave like ownership and not like symbolism wrapped in legal structure. South Africa’s most interesting answer to wage inequality may not have been in payroll at all, but in the attempt to widen participation in the asset. Even there, though, the distance between legal inclusion and durable wealth creation has proved stubborn.[8]

A Fairer Model Would Not Abolish Incentives

This is where the debate usually goes wrong. The choice is not between executive capitalism and envy. Nor is it between paying CEOs badly and paying them well. The real question is whether South African firms can justify globally benchmarked executive rewards while relying on a weakly shared domestic wage structure below. A fairer model would still use incentives, but it would ask harder questions of them. How much reward came from management skill and how much from the cycle? How much upside reaches employees beyond the executive tier? How much disclosure is comparable enough to matter? And why is internal pay legitimacy still treated as a communications issue rather than a strategic one?[2, 3]

Boards will keep saying the market for executives is global. In one sense, they are right. But that is precisely the tension. South Africa has built a dual compensation regime: executives priced against global capital markets, workers priced against a weak local labour market. That is not a neutral outcome. It is an institutional choice.[1, 3]

The Ledger View

- What the ratio measures: CEO-worker multiples are not only about compensation. They are a visible map of bargaining power inside the firm.

- The structural problem: South Africa often prices executives globally while workers remain tied to a weak local wage structure.

- The macro twist: In cyclical sectors, executive rewards can rise on the back of boom conditions that no individual manager fully controls.

- The unresolved question: Can South African capitalism remain legitimate if reward keeps concentrating at the top while the wage base below stays this weak?

The Real Divide

The divide between Nordic economies and emerging ones is not simply what they pay at the top. It is how seriously they shape what happens beneath it. South Africa has sophisticated listed firms, complex remuneration structures and growing disclosure pressure, yet still struggles to convert that into a shorter and more legitimate ladder. The problem is not that the country lacks performance pay. It is that performance is measured more generously at the top than it is shared below.[3, 4]

CEO pay is never just about what one executive deserves. It is a referendum on how far a society is willing to let the ladder stretch before it starts to doubt the system itself.

References

- Deloitte South Africa. 2020. “CEOs feel the pinch as COVID-19, environmental and social matters bite.” Public summary of South African executive remuneration trends.

- PwC South Africa. 2025. “2025 Directors Remuneration and Trends Report.” Public report summary on JSE executive pay trends.

- Just Share. 2024. “Pay gaps and leadership diversity in the JSE-listed wholesale and retail sector.”

- OECD. 2025. “OECD Corporate Governance Factbook 2025” and related governance materials on long-term incentives; plus Nordic labour-market background from comparative wage-bargaining literature.

- Statistics South Africa. 2015. Quarterly Employment Statistics (QES), December 2015. Average monthly earnings in the formal non-agricultural sector: R17,517 in November 2015.

- Statistics South Africa. 2025. Quarterly Employment Statistics (QES), March 2025. Average monthly earnings in the formal non-agricultural sector: R28,289 in February 2025.

- News24. 2025. Public reporting on PwC’s 2025 remuneration findings, including a median CEO total remuneration figure of roughly R22.3 million.

- MultiChoice / Phuthuma Nathi investor materials and company updates describing shareholder participation and cumulative dividends.